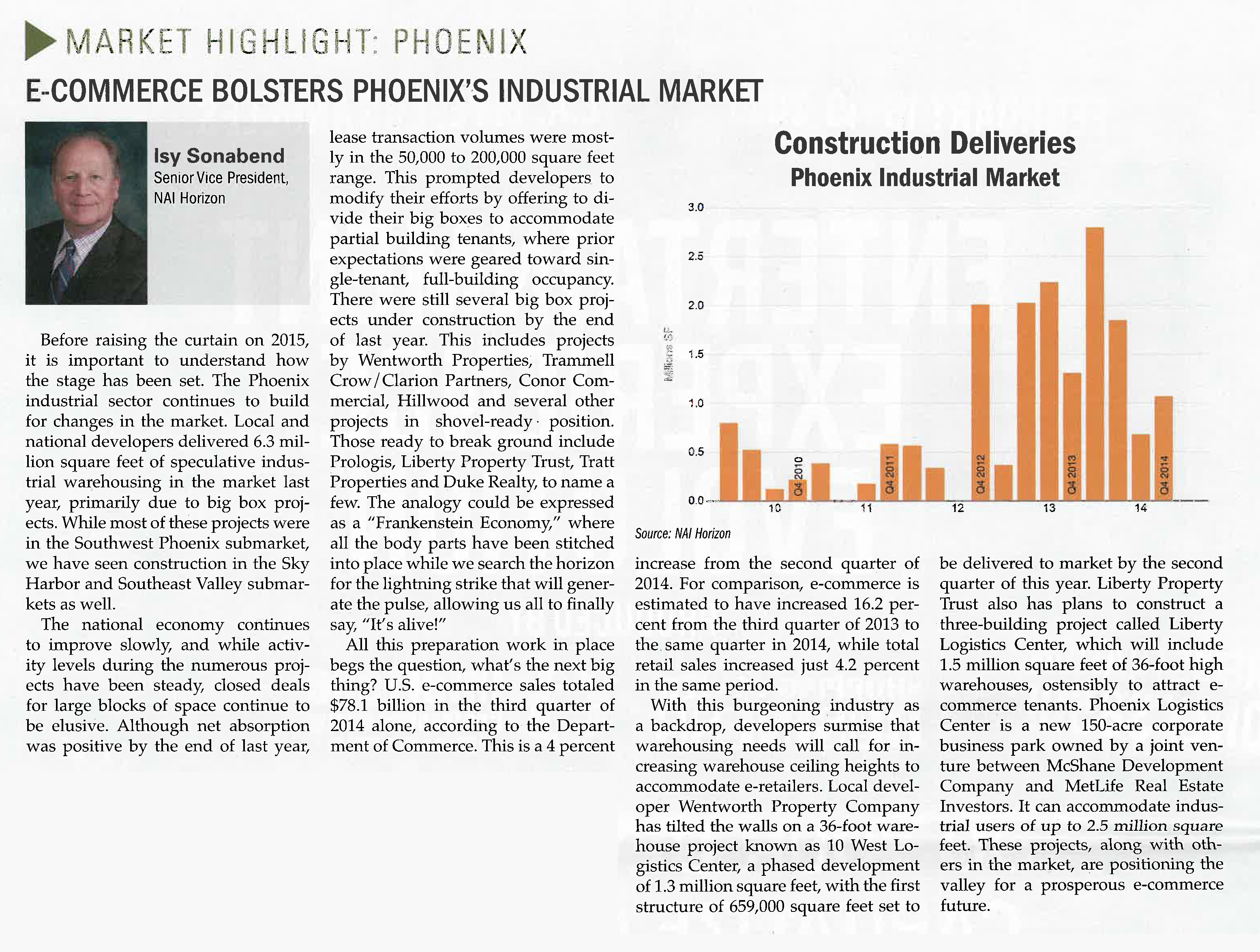

Prepared by John S. Filli, SIOR

Date prepared: April 14, 2014

Overall, Office and Industrial Markets across the country experienced slightly different performance levels in 2013. The combined Fourth Quarter 2013 Commercial Real Estate Index advanced from 93.7 to 96.4 ——- up 2.7 points from the Third Quarter 2013 (a score of 100 indicates a balanced market) and the highest value since the Fourth Quarter 2007. Bolstered by brisk international trade and positive consumer spending, the industrial sector posted solid demand for space resulting in declining vacancies and rising rental rates as is evidenced by the combined CREI industrial component achieving a value of 103 (up 3.9 points from the previous quarter). This indicates that the industrial sector is experiencing markedly improving fundamentals (i.e. increased demand for warehousing due to larger international trade volume). Office markets, on the other hand, experienced softer demand due to employment trends not hitting their stride as is evidenced by the CREI office component achieving a value of 85.7 points (down 0.3 points from the previous quarter).

During the Fourth Quarter 2013, positive growth was present across all four major regions of the country with the South and Midwest leading the way with index values of 104.6 and 94.2, respectively . Looking ahead toward the remainder of 2014, SIOR respondents to the survey expect the outlook for commercial real estate to slightly improve (77% of those surveyed indicated growth in the 1-15% range). As capital from both domestic and global investors continues to enter the market, it should disperse in a wider geographic pattern. Furthermore, as the economy strengthens and grows, performance of underlying assets should boost values and, in turn, lead to increased capital liquidity across all property types. In weighing the results of the SIOR Index for the Fourth Quarter 2013 against those of a year ago, it is evident that commercial markets have continued to make noticeable strides. Although both Office and Industrial markets are still working through lingering challenges, signals continue to point toward steady improvement.

Leasing, Investment, and Sales Activity

Overall leasing activity continued to expand during the quarter, with practitioners reporting declining vacancy rates—-69 percent of SIORs surveyed indicated that vacancies are lower than a year ago. Most respondents to the survey (93%) reported steady or rising rents. However, slightly over half of the practitioners reported rents in line with or slightly above long-term averages. In addition, subleasing availability also declined, with only 8 percent of SIORs reporting ample sublease space. As landlord concessions continue to decline, markets are beginning to turn in favor of the landlord.

Construction and Development

New construction of office and industrial spaces showed an increase in the fourth quarter, with 15 percent of respondents reporting volumes rising above historical averages (compared with 12 percent the prior quarter).

Development conditions were on an upward swing, with 46 percent of SIOR members surveyed finding it a Buyer’s market. Investment prices remained moderate—lower than construction costs in 65 percent of the markets.

SIOR Outlook

Based on the results of the fourth quarter survey, commercial markets continue to ramp up, following the gains recorded during the prior quarter. SIOR members expect conditions to improve moving forward through 2014, with 77 percent of respondents expecting growth in the 1-15 percent range.

Overview and Derivation of the SIOR Commercial Real Estate Index as provided by the Society of Industrial and Office Realtors (SIOR)

“The index is based on an electronic survey/questionnaire with 10 topics sent out to SIOR members nationwide. The topics covered are (1) recent leasing activity, (2) trends in asking rents, (3) trends in vacancy rates, (4) subleasing conditions, (5) levels of concession packages in leases, (6) development activity, (7) site acquisition activity, (8) investment pricing levels, (9) the impact of the local economy on the property market, and (10) the effect of the national economy on the property market. For each topic, five choices are provided, corresponding to conditions that are very weak, moderately weak, well-balanced, moderately strong, or very strong.

For each question, answers are tallied and the percentage of responses for each of the five choices is calculated. If survey panelists indicate “very weak” conditions (the “a” choices in the questionnaire), the answer is assigned 0 (zero) points ; “moderately weak” (“b” answers) earn 5 points; an indication of “market balance” (“c”) receives 10 points; “moderately strong” indications (“d”) score 15 points; and “very strong” (“e”) responses receive a maximum 20 points. Thus a score of 10 for a given question can be earned if responses are evenly distributed across all five choices, if all responses were “c”, or if the answers form a “bell-shaped curve” centered around the “c” choice. The total index value is derived by summing the scores for all 10 questions. Index values for each of the two property types are similarly calculated.

The SIOR Commercial Real Estate Index is constructed as a “diffusion index”, a very common and familiar indexing technique for economic measures. Other examples of diffusion indexes include the Index of Leading Economic Indicators, The Consumer Confidence Index, and the Institute of Supply Management’s Purchasing Managers’ Index. In the SIOR Commercial Real Estate Index, a value of 100 represents a well balanced market for industrial and office property. Values significantly lower than 100 indicate weak market conditions. The theoretical limits of the index are a low of zero, and a high of 200, though it is unlikely that such limits would be approached as long as the property markets are operating efficiently.”

The questionnaire and index were devised for SIOR by Hugh F. Kelly, CRE. Hugh is the principal of Hugh Kelly Real Estate Economics and a clinical associate professor of real estate at New York University.

For more information or to view the full report including: Arizona Market Trends, China’s Impact on Arizona’s Economy, and Forecasts, please contact John Filli, SIOR.