Setting the Stage for a Sustainable 2013

With the bottom in the rearview mirror, the Phoenix industrial market is continuing its strong climb back to pre-recession standards. With vacancy continuing to decline, and with construction on the rise, 2013 will elevate the sector towards its previous levels of growth and expansion. Construction employment in Arizona jumped 7.3% in February from a year ago, adding 8,300 new construction jobs statewide, ranking Arizona as the fifth highest in the nation. This activity in the Valley bodes well for the industrial market and aligns with the recovery the industrial sector is experiencing.

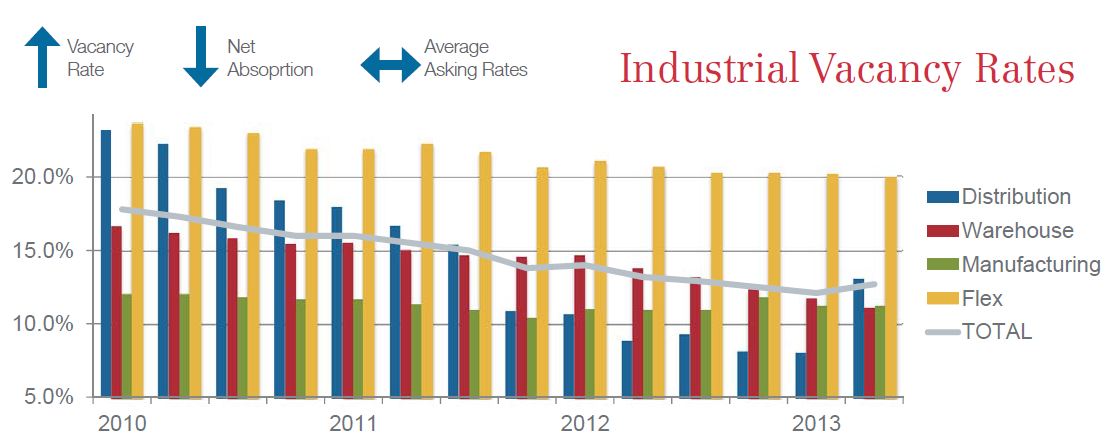

Vacancy fell to 11.9% in Q1 of 2013, down from 12.4% at YE 2012, and down remarkably from Q1 of 2012, when the rate sat at 14%. This trend is expected to continue as we see the market adjusting back to previous indices. While we may not see vacancy drop to the historical lows of 2006 for some time, when rates hovered between 7%-8%, the sector is close to resetting the clock to 2007/2008 levels when vacancy rates hovered around 10% before the recession hit the economy hard. Absorption numbers also remain steady; while down over a million SF from Q4 2012, Q1 posted a substantial net positive absorption of 1,564,392 SF. Q1 2013 absorption posted the strongest first quarter seen in 6 years. All five industrial submarkets posted positive absorption numbers with the Northwest Valley and Southeast Valley leading the way with over a million SF combined.

Construction and deliveries have continued to ramp up over the past two years. 2013 began with over 5 million SF under construction in 15 projects. Just two years ago, Q1 2011 showed only 450,000 SF under construction and has been steadily increasing since then. Deliveries have also been on the rise for the past two years, showing signs of increased confidence. While down from the impressive YE 2012 of over 2 million SF delivered, Q1 2013 started off strong with 447,792 SF of new construction. The largest project this year comprising a majority of the total delivered SF is 2 S Price Road, a 350,000 SF class B industrial telecom hotel/data hosting building situated in the Price Road corridor of the Southeast submarket.

Rental rates continue to remain flat, increasing only slightly this quarter to $0.51 per SF monthly. As 2013 begins to take shape and the industrial sector moves forward in its recovery, it is anticipated that there will be a corresponding increase in rental rates.

The top sale transactions for this year include 3200 W Germann Rd., Chandler, a 125,000 SF Class B Manufacturing Building that sold for an allocated $13,072,447, and 1830-1850 N 95th Ave., Phoenix, a multi-property sale of three flex buildings with a total RBA of 118,853 SF for $12.7 million. The top lease transactions for the quarter included 6725 W Allison Rd., Chandler, a 105,000 SF lease to Sound Packaging, and 5120 W Buckeye Rd., Phoenix, a 80,587 SF lease to Amcor Packaging.